|

|

Corporation Tax Increase 2023 – What does it mean for your business and how to reduce your tax bill?

Palma Percze

In the budget in March 2021, it was announced that Corporation Tax would be increased incrementally to 25%. After some uncertainty in the past year, as to whether this would proceed, the first increase took effect from 1 April 2023.

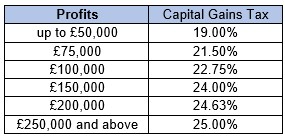

The increase will affect companies (and unincorporated associations) with profits of £250,000 or more, whilst companies with profits up to £50,000 will benefit from the introduction of the small profits rate, which means that they will continue to pay tax at 19%. If profits are in excess of £250,000, the new rate of 25% will apply to all profits, including those below the £250,000 threshold.

The rate of corporation tax applicable to companies with profits between £50,000 and £250,000 is set out below.

Companies whose accounting periods ends soon after April 2023 will pay a pro-rata corporation tax rate. The bands may also be proportionately reduced by the number of associated companies a company has. If a company has one or more ‘associated companies’ then the thresholds for determining the applicable tax rate and any marginal relief are divided by the total number of associated companies.

For clarity, a company is classed as an associated company of another company if one has control of the other, or both are under the control of the same person or persons. However, for corporation tax purposes dormant companies are not deemed to be associated companies. In addition to this, being part of a group could mean that choosing to offset an amount overpaid by one company against an amount unpaid by another company in the group could be an option.

On another positive note, the increase of corporation tax will not have an effect on the Annual Investment Allowance. The government has announced that the AIA of £1 million, which was initially only a temporary increase from the previous £200,000 allowance, is due to be set permanent from 1 April 2023. The AIA allows a business to deduct the total amount of qualifying capital expenditure up to the £1 million limit from its taxable profits in a given tax year. This allowance is primarily designated for the purchase of business equipment, tools, and machinery.

Companies that are struggling to pay their increased tax bill may wish to take advantage of the Time to Pay arrangement with HMRC and set up a payment plan. In order to reduce their corporation tax liability companies may also wish to consider the following:

- Extracting profit from the company by way of salary, dividends, loans and pension contributions;

- The impact of associated companies and whether restructuring would be beneficial;

- Paying corporation tax early and claiming interest from HMRC for early payment. The current interest rate for early payment is 0.5%; and

- Where losses are made, whether it would be more beneficial to carry them forward to benefit at a higher rate in the future rather than carry them back.

Contact us

If you require any assistance or further information with the information discussed in this article, please do not hesitate to contact Jon Davage, Partner at Bermans at jon.davage@bermans.co.uk or call 0161 827 4600.